More efficient or more volatile? The adoption of the latest iterations of artificial intelligence by financial markets can improve risk management and deepen liquidity; but it could also make markets opaque, harder to monitor, and more vulnerable to cyber-attacks and manipulation risks.

The new Global Financial Stability Report looks at new market data to understand where this technology might be taking us. IMF staff conducted extensive outreach across various stakeholders—from investors to technology providers to market regulators—to show how financial institutions are harnessing advances in AI for capital market activities, and the potential impact of its adoption.

Hedge funds, investment banks, and others have been using quantitative trading strategies for decades. Automated trading algorithms have helped markets move faster and digest large trades more efficiently in major asset classes such as US equities. But they have also contributed to “flash crash” events when market prices have swung wildly in very short periods of time—such as in May 2010 when US stock prices collapsed only to rebound minutes later—and there are fears they could destabilize markets in times of severe stress and uncertainty.

Artificial intelligence, through its ability to almost instantly process large amounts of data and even text for use by traders, is poised to take these kinds of changes to another level. However, while generative AI and other recent breakthroughs are attracting attention in both the popular press and in financial markets, today they are used in only limited ways by actual investors. So, if we are only at the beginning of an AI-led transformation, where might we be headed?

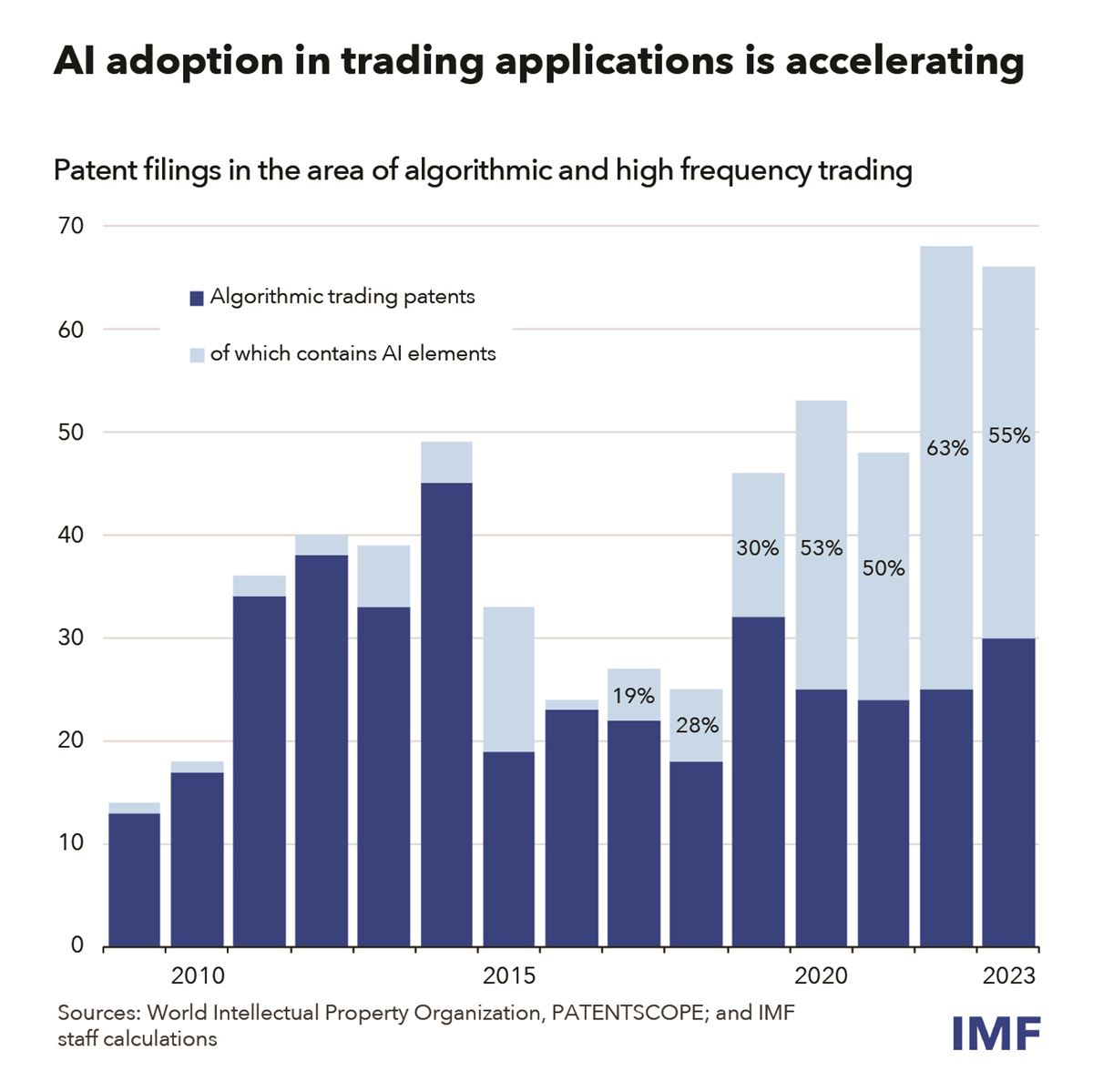

Patent filings are a good way to understand this, given what is often a long lead time between filings and actual production-ready technology. Since large language models, or LLMs, started to appear in 2017, the share of AI content in patent applications related to algorithmic trading has risen from 19 percent in 2017 to over 50 percent each year since 2020, suggesting a wave of innovation is coming in this area.

These new innovations will likely further AI's ability to quickly rebalance investment portfolios, which will in turn lead to higher trading volumes. Market participants we surveyed concur that high-frequency, AI-driven trading is expected to become more prevalent, particularly in liquid asset classes like equities, government bonds, and listed derivatives. They foresee greater integration of sophisticated AI in investment and trading decisions within three to five years, although a “human in the loop” approach is expected to persist, especially for large capital allocation decisions.

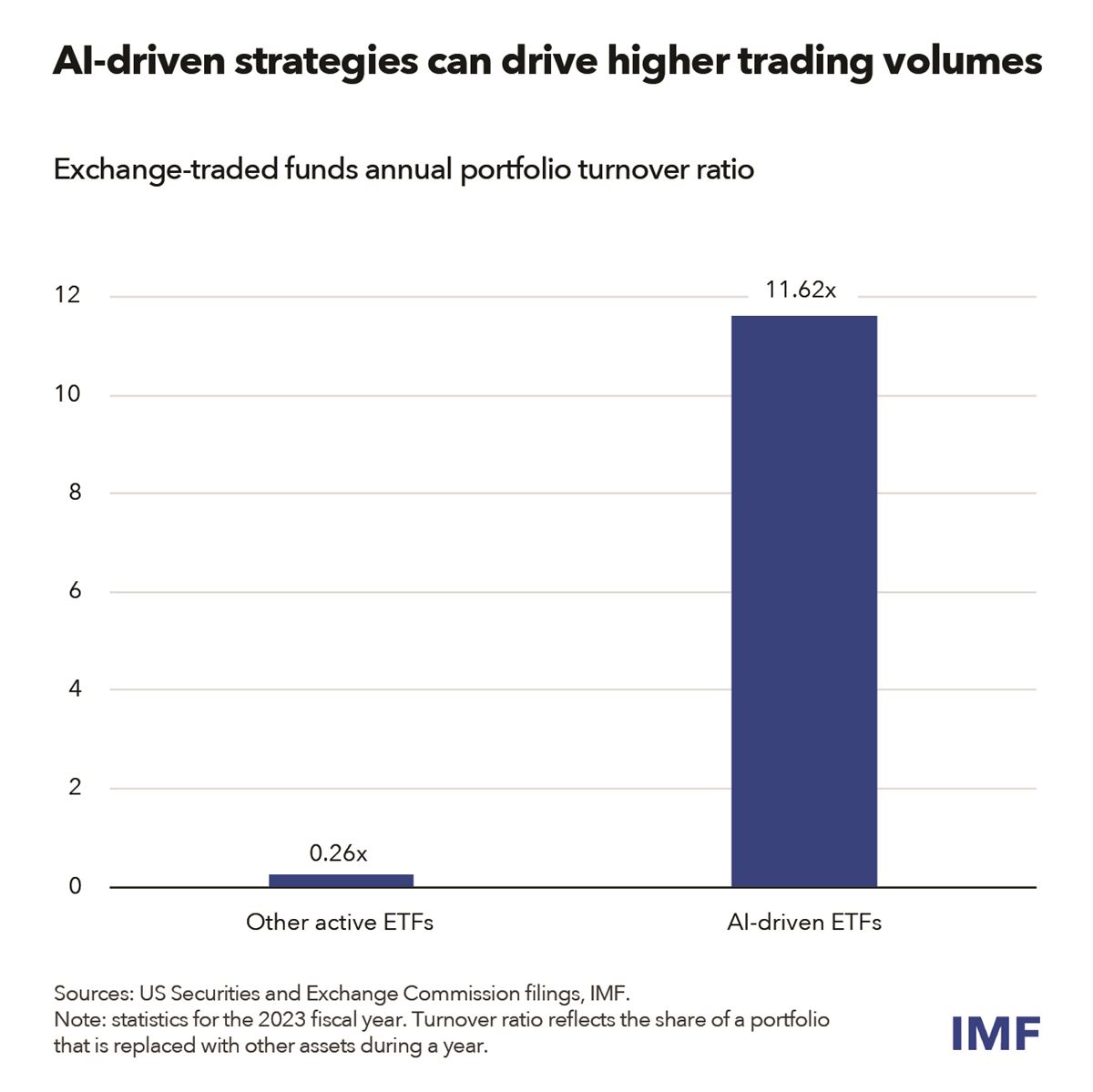

Evidence of these changes is already being seen in the exchange-traded fund market. Although currently small, AI-driven ETFs show a significantly higher turnover compared to other ETFs. While a typical actively managed equity ETF turns over its holdings much less than once a year, AI-driven ETFs do so about once a month. If widespread, such strategies may in the future mean deeper, more liquid markets which are good for investors. But they could also contribute to market instability: several AI-driven ETFs saw increased turnover during the March 2020 market turmoil, suggesting the potential for increased herd-like selling during times of stress.

Prices may react much more quickly in an AI-driven market. Investors mentioned the release of the complex and lengthy minutes of Federal Reserve meetings as an example where AI could provide a trading signal faster than any human trader could, and this may already be happening. Since 2017 and the introduction of LLMs, the movement of US equity prices 15 seconds after the release of the Fed minutes seem to be more consistently in the direction of the longer-lasting movement seen after 15 minutes, in contrast to the apparently uncorrelated movements in the pre-LLM period.

Who will be able to take advantage of these new technologies? AI might lead to a further migration of investment to hedge funds, proprietary trading firms, and other nonbank financial intermediaries, which would make markets less transparent and harder to monitor. Nonbanks have a structural advantage in the adoption of AI. They are generally more agile and subject to fewer regulatory constraints than large commercial and investment banks, which often must deal with legacy infrastructure and may be subject to more stringent requirements, including ensuring the explainability of complex AI models.

Policy recommendations

How should regulators and supervisors prepare for this new world? In a faster reacting market where nonbanks may continue to rise in importance, various aspects of regulation and supervision in AI-related areas should be enhanced.

Financial sector authorities and trading venues should determine if they need to design new volatility response mechanisms—or modify the existing ones appropriately—to respond to “flash crash” events potentially originated in AI-driven-trading. These include margin requirements, circuit breakers, and the resilience of central counterparties.

Similarly, financial sector authorities should continue to strengthen oversight and regulation of nonbank financial intermediaries by requiring them to identify themselves and disclose AI-relevant information; as well as require financial institutions to regularly map interdependencies between data, models, and technological infrastructure supporting AI models.

A close monitoring and oversight of this rapidly changing market lays the foundation for an opportune and balanced regulatory response that may allow financial sector participants to benefit from AI while mitigating its risks.

—This blog is based on Chapter 3 of the October 2024 Global Financial Stability Report, “Advances in Artificial Intelligence: Implications for Capital Market Activities.”